Cold Spray Technology Market Size, Growth, Trends | Report 2023-2032

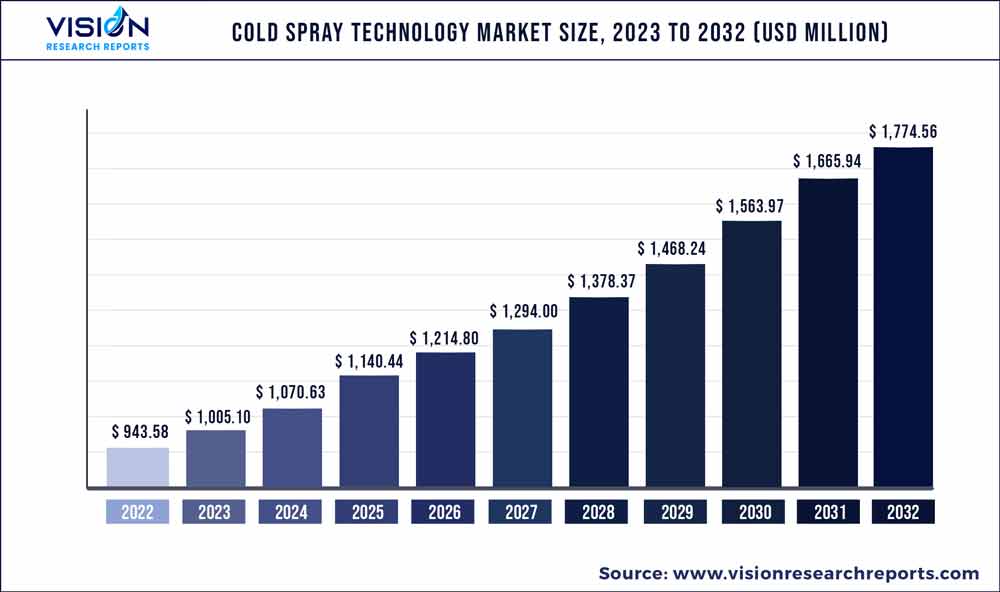

The global cold spray technology market was valued at USD 943.58 million in 2022 and it is predicted to surpass around USD 1,774.56 million by 2032 with a CAGR of 6.52% from 2023 to 2032.

Key Pointers

Report Scope of the Cold Spray Technology Market

| Report Coverage | Details |

| Market Size in 2022 | USD 943.58 million |

| Revenue Forecast by 2032 | USD 1,774.56 million |

| Growth rate from 2023 to 2032 | CAGR of 6.52% |

| Base Year | 2022 |

| Forecast Period | 2023 to 2032 |

| Market Analysis (Terms Used) | Value (US$ Million/Billion) or (Volume/Units) |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Companies Covered | ASB Industries (Hannecard Roller Coatings; Inc); Bodycote plc; Flame Spray Technologies BV; Plasma Giken Co., Ltd.; VRC Metal Systems; CenterLine (Windsor) Limited; WWG Engineering Pte. Ltd.; Praxair S.T. Technology, Inc.; Impact Innovations GmbH; Concurrent Technologies Corporation; Effusiontech Pty Ltd (SPEE3D); Titomic Limited |

The rising demand from aerospace industry and growing electrical & electronics industry will drive the market demand in the forecast period.

Cold spray coating, especially in the aerospace industry has revolutionized component repairing. The utilization of cold spray coating technology improves the thermal stability and corrosion resistance of materials and ensures increased reliability for an extended time. In addition, it offers protection against extreme temperatures, harsh environments, and extends the lifespan of the components. These aforementioned factors will drive the product demand for aerospace industry in the coming years.

Furthermore, the increasing number of air passengers coupled with the increase in tourism, business travel, and air freight travel has led to the expansion of aerospace industry. For instance, according to the World Tourism Barometer of the UN World Tourism Organization, the number of foreign visitors almost quadrupled from January to July 2022 (+172%) compared to the same period in 2021. New airports are being constructed across the world, and the subsequent demand for new aircraft is continuously increasing.

In electrical & electronics industry, cold spray coating technology is used to coat electrical components with copper, tantalum, titanium, and aluminum. Various components such as circuit boards, electrical contacts, semiconductors, electric motors, and generators are coated using cold spray coating technology. The coating of such parts with metals and metal alloys provides the components with better electrical conductivity, corrosion resistivity, and clearance control. These aforementioned factors will drive the demand in the forecast period.

Expenditure on personal electronic devices, medical devices, and consumer electronics is rising owing to the increased disposable income, production of affordable devices, and increased accessibility of products. According to the Groupe Speciale Mobile Association (GSMA), by the end of 2021, around 5.3 billion people were subscribed to mobile connections, which represented 67% of the population worldwide. Mobile technologies and services generated approximately USD 4.5 trillion of economic value added in 2021, which is anticipated to reach USD 5 trillion by 2025. Thus, the growing electrical & electronics industry will drive the demand in the forecast period.

Manufacturers are undertaking mergers & acquisitions, and product launches to strengthen their geographical presence. For instance, in November 2022, Titomic Limited launched D623 medium-pressure cold spray additive manufacturing (AM) machine. The D623 machine can deposit much harder metals than the compared to D523 lower compression system. The D623 provides higher restoration of high-wear parts and wear-resistant coatings.

Material Insights

The aluminum segment led the market and accounted for 30.63% of the global revenue share in 2022. Cold-sprayed aluminum alloys have exceptional characteristics and have drawn the interest of numerous researchers in addition to pure aluminum. For instance, alloys made of aluminum and silicon offer great strength, minimal thermal expansion, and superior anti-friction characteristics. Additionally, there are other advantages to cold spraying aluminum, including improved bonding and strength comparable to the bulk material. It also supports a wide range of applications in component repair, additive manufacturing, and marine industry.

Copper cold spraying has remarkable thermal conductivity, electrical conductivity, ductility, corrosion resistance, and wear resistance. Copper and its alloys find extensive usage in a variety of industries, including machinery, electronics, and electric power, and other energy-related disciplines. Given their ease of deposition, they are frequently employed as the model material in investigations of cold spray. These aforementioned factors will drive the demand for copper material in cold spray technology.

Several advantages of cold spraying nickel are its resistance to hot gases, energetic material coatings, and high temperature corrosion. Furthermore, nickel has diverse capabilities and features such as accidental collision, overhaul, or inappropriate operation. Additionally, a wide number of applications, including those in the aerospace, automotive, glass, medical, agricultural, roller mill, hydraulic pump, and component repair industries, are served by cold spraying nickel. These aforementioned factors will drive the nickel material demand.

The titanium segment is expected to exhibit a CAGR of 7.54% in the forecast period. Titanium is utilized extensively in petroleum, aviation, chemical, medical, sports equipment, and construction, aerospace, automotive, and other fields owing to its high strength, good biocompatibility, superior corrosion resistance, and low density.

Service Insights

The cold spray coatings segment led the market and accounted for 95.93% of the global revenue share in 2022. Cold spray coatings prevent tensile residual stresses, oxidation, and undesirable chemical reactions. Furthermore, the latest technique for depositing coatings and carrying out additive manufacturing of structures is cold spraying. Different metallic or metallic-ceramic materials can be used in this low-temperature procedure to create coatings with a quality that is not possible to achieve using any other method These aforementioned factors will propel the demand for cold spray coatings in the coming years.

Cold spray coatings, a cutting-edge coating technique, rely on kinetic energy when they are blasted at extremely high pressures. Since cold spray uses kinetic energy instead of thermal energy for deposition, it has various technological benefits over the thermal spray process when it comes to coating surfaces.

The cold spray additive manufacturing (CSAM) segment is expected to exhibit a CAGR of 16.87% in the forecast period. It is a high-potential, newly developed technology used for the development of engineering components that offer improved performance across a variety of surfaces, sub surfaces, and interfaces. The majority of the recent developments in cold spray additive manufacturing technology have been focused on electric motors used in the automotive industry to reduce carbon dioxide emissions from automobiles wherein these motors are to be used.

Efforts are being made to make these motors highly efficient, light, and cost-effective with the use of cold spray additive manufacturing technology. These aforementioned factors will drive the demand for cold spray additive manufacturing service over the forecast period. For instance, the National Research Council of Canada adopted CSAM technology to generate permanent magnets for electric motors. The motors developed using this technology are expected to be compact and offer high performance. Thus, the benefits offered by CSAM technology are anticipated to fuel its adoption worldwide during the forecast period.

End-use Insights

The aerospace end-use segment led the market and accounted for 28.22% of the global revenue share in 2022. It is also used in aerospace sector in a variety of components including satellites, gearboxes, landing gear nozzles, engine parts, and other nonstructural elements. These components are shielded from severe temperatures by cold spray technology, which guarantees enhanced dependability over time. It has minimal porosity, great bonding, and an oxide-free coating in solid state and at low temperatures, making it suited for use in aerospace industry.

Utility segment include power boilers, gas and hydro-steam turbines, turbochargers, and nuclear & solar heat & solar energy. These type of machinery comprises various components including turbine buckets, turbine nozzles, turbine rotors, compressor wheels, compressor blades, and combustion baskets, which are used in harsh environments and under high mechanical & temperature loads. Harsh operating conditions may cause fatigue, corrosion, creep, and wear damage to the components, which necessitates proper maintenance and repair of the components for their long-run application.

Cold spray technology is used in automotive industry to repair a number of parts including heated glass, valve seats, turbochargers, crankshafts, braking discs, bearings, exhaust systems, and crankshafts. By preventing wear, corrosion, fretting, and erosion, the use of cold spray technology prolongs component life and enhances vehicle performance. In automotive sector, the criteria for emission limitations are getting stricter. Modern cars can reduce their exhaust gas emissions owing to enhanced emission control. Due to stricter and increasing environmental rules, emissions from brake wear, such as particulate matter and brake dust, are becoming a rising concern for automotive industry. As a result, the above-mentioned emission limitations and environmental rules, cold spray technology is utilized to eliminate significant emissions, poor corrosion resistance, and excessive wear, thereby, driving the demand for the market over the forecast period.

The electrical and electronics segment is expected to exhibit a CAGR of 7.49% over the forecast period. Due to its expanding use in a variety of components such as electrical contacts, refrigeration units, circuit boards, electric motors & generators, transformers, semiconductors & displays, and bus bars, which require high electrical resistance, corrosion resistance, and oxidation resistance to operate in harsh environments, cold spray coating is experiencing increased demand in electrical & electronics end-use sector. These aforementioned factors will drive the demand for cold spray technology for electrical and electronics in the coming years.

Regional Insights

North America led the market and accounted for over 41.24% of the global revenue in 2022. The demand for cold spray technology in North America is driven by its flourishing aerospace & defense, electronics, and automotive industries. Moreover, ongoing research activities to explore the application of cold spray technology for damage and dimensional repair of various components used in military aircraft and vehicles, as well as in marine vessels is projected to drive the growth of the market in North America over the forecast period. For instance, in 2019, Worcester Polytechnic Institute (WPI) announced that it received a grant of USD 25 million from the U.S. Army Combat Capabilities Development Command Army Research Laboratory to develop a cold spray additive manufacturing technology for repairing and manufacturing metal parts

Europe represents the second-largest market for cold spray technology globally owing to the presence of modern infrastructure and facilities, increased research & development activities, and the availability of a highly qualified workforce. The recent development of cold spray applications for repair and additive manufacturing of various components in different fields including biomedical, aerospace, electronics, energy, and semiconductor is projected to drive the market over the forecast period.

Asia Pacific is estimated to witness a CAGR of 7.21% over the forecast period. A high concentration of electronic companies in China, South Korea, Japan, and Taiwan is expected to offer sustainable growth opportunities for cold spray manufacturers over the forecast period.

Furthermore, favorable initiatives such as Digital India and Make in India undertaken by the Government of India are expected to drive the production of electronic devices in the country over the foreseeable future. Thus, with the growing electrical & electronics industry, the demand for circuit boards, electrical contacts, electric motors & generators, and semiconductors & displays is also rising, as majority of these components are utilized during the manufacturing of electronic products. The cold spray coating offers excellent thermal stability, heat resistance, corrosion resistance, oxidation resistance, and electrical resistance properties, which help in extending the working life of electrical and electronics components, thereby driving market demand.

The Central & South American cold spray technology market is expected to witness significant growth owing to increasing industrial investments in the automotive sector. Major manufacturers such as Volkswagen, and General Motors, announced the expansion of their existing manufacturing facilities in the region to cater with the increasing demand. Furthermore, the growth in the consumption of home appliances, owing to rapid urbanization, technological innovations, and increased disposable incomes of consumers in the region, is expected to propel the demand for cold spray technology over the projection period.

Cold Spray Technology Market Segmentations:

By Material

By Service

By End-use

By Regional

Chapter 1. Introduction

1.1. Research Objective

1.2. Scope of the Study

1.3. Definition

Chapter 2. Research Methodology

2.1. Research Approach

2.2. Data Sources

2.3. Assumptions & Limitations

Chapter 3. Executive Summary

3.1. Market Snapshot

Chapter 4. Market Variables and Scope

4.1. Introduction

4.2. Market Classification and Scope

4.3. Industry Value Chain Analysis

4.3.1. Raw Material Procurement Analysis

4.3.2. Sales and Distribution Material Analysis

4.3.3. Downstream Buyer Analysis

Chapter 5. COVID 19 Impact on Cold Spray Technology Market

5.1. COVID-19 Landscape: Cold Spray Technology Industry Impact

5.2. COVID 19 - Impact Assessment for the Industry

5.3. COVID 19 Impact: Global Major Government Policy

5.4. Market Trends and Opportunities in the COVID-19 Landscape

Chapter 6. Market Dynamics Analysis and Trends

6.1. Market Dynamics

6.1.1. Market Drivers

6.1.2. Market Restraints

6.1.3. Market Opportunities

6.2. Porter’s Five Forces Analysis

6.2.1. Bargaining power of suppliers

6.2.2. Bargaining power of buyers

6.2.3. Threat of substitute

6.2.4. Threat of new entrants

6.2.5. Degree of competition

Chapter 7. Competitive Landscape

7.1.1. Company Market Share/Positioning Analysis

7.1.2. Key Strategies Adopted by Players

7.1.3. Vendor Landscape

7.1.3.1. List of Suppliers

7.1.3.2. List of Buyers

Chapter 8. Global Cold Spray Technology Market, By Material

8.1. Cold Spray Technology Market, by Material, 2023-2032

8.1.1 Nickel

8.1.1.1. Market Revenue and Forecast (2020-2032)

8.1.2. Copper

8.1.2.1. Market Revenue and Forecast (2020-2032)

8.1.3. Aluminum

8.1.3.1. Market Revenue and Forecast (2020-2032)

8.1.4. Titanium

8.1.4.1. Market Revenue and Forecast (2020-2032)

8.1.5. Magnesium

8.1.5.1. Market Revenue and Forecast (2020-2032)

8.1.6. Others

8.1.6.1. Market Revenue and Forecast (2020-2032)

Chapter 9. Global Cold Spray Technology Market, By Service

9.1. Cold Spray Technology Market, by Service, 2023-2032

9.1.1. Cold Spray Additive Manufacturing

9.1.1.1. Market Revenue and Forecast (2020-2032)

9.1.2. Cold Spray Coatings

9.1.2.1. Market Revenue and Forecast (2020-2032)

Chapter 10. Global Cold Spray Technology Market, By End-use

10.1. Cold Spray Technology Market, by End-use, 2023-2032

10.1.1. Aerospace

10.1.1.1. Market Revenue and Forecast (2020-2032)

10.1.2. Automotive

10.1.2.1. Market Revenue and Forecast (2020-2032)

10.1.3. Defense

10.1.3.1. Market Revenue and Forecast (2020-2032)

10.1.4. Electrical & Electronics

10.1.4.1. Market Revenue and Forecast (2020-2032)

10.1.5. Utility

10.1.5.1. Market Revenue and Forecast (2020-2032)

10.1.6. Others

10.1.6.1. Market Revenue and Forecast (2020-2032)

Chapter 11. Global Cold Spray Technology Market, Regional Estimates and Trend Forecast

11.1. North America

11.1.1. Market Revenue and Forecast, by Material (2020-2032)

11.1.2. Market Revenue and Forecast, by Service (2020-2032)

11.1.3. Market Revenue and Forecast, by End-use (2020-2032)

11.1.4. U.S.

11.1.4.1. Market Revenue and Forecast, by Material (2020-2032)

11.1.4.2. Market Revenue and Forecast, by Service (2020-2032)

11.1.4.3. Market Revenue and Forecast, by End-use (2020-2032)

11.1.5. Rest of North America

11.1.5.1. Market Revenue and Forecast, by Material (2020-2032)

11.1.5.2. Market Revenue and Forecast, by Service (2020-2032)

11.1.5.3. Market Revenue and Forecast, by End-use (2020-2032)

11.2. Europe

11.2.1. Market Revenue and Forecast, by Material (2020-2032)

11.2.2. Market Revenue and Forecast, by Service (2020-2032)

11.2.3. Market Revenue and Forecast, by End-use (2020-2032)

11.2.4. UK

11.2.4.1. Market Revenue and Forecast, by Material (2020-2032)

11.2.4.2. Market Revenue and Forecast, by Service (2020-2032)

11.2.4.3. Market Revenue and Forecast, by End-use (2020-2032)

11.2.5. Germany

11.2.5.1. Market Revenue and Forecast, by Material (2020-2032)

11.2.5.2. Market Revenue and Forecast, by Service (2020-2032)

11.2.5.3. Market Revenue and Forecast, by End-use (2020-2032)

11.2.6. France

11.2.6.1. Market Revenue and Forecast, by Material (2020-2032)

11.2.6.2. Market Revenue and Forecast, by Service (2020-2032)

11.2.6.3. Market Revenue and Forecast, by End-use (2020-2032)

11.2.7. Rest of Europe

11.2.7.1. Market Revenue and Forecast, by Material (2020-2032)

11.2.7.2. Market Revenue and Forecast, by Service (2020-2032)

11.2.7.3. Market Revenue and Forecast, by End-use (2020-2032)

11.3. APAC

11.3.1. Market Revenue and Forecast, by Material (2020-2032)

11.3.2. Market Revenue and Forecast, by Service (2020-2032)

11.3.3. Market Revenue and Forecast, by End-use (2020-2032)

11.3.4. India

11.3.4.1. Market Revenue and Forecast, by Material (2020-2032)

11.3.4.2. Market Revenue and Forecast, by Service (2020-2032)

11.3.4.3. Market Revenue and Forecast, by End-use (2020-2032)

11.3.5. China

11.3.5.1. Market Revenue and Forecast, by Material (2020-2032)

11.3.5.2. Market Revenue and Forecast, by Service (2020-2032)

11.3.5.3. Market Revenue and Forecast, by End-use (2020-2032)

11.3.6. Japan

11.3.6.1. Market Revenue and Forecast, by Material (2020-2032)

11.3.6.2. Market Revenue and Forecast, by Service (2020-2032)

11.3.6.3. Market Revenue and Forecast, by End-use (2020-2032)

11.3.7. Rest of APAC

11.3.7.1. Market Revenue and Forecast, by Material (2020-2032)

11.3.7.2. Market Revenue and Forecast, by Service (2020-2032)

11.3.7.3. Market Revenue and Forecast, by End-use (2020-2032)

11.4. MEA

11.4.1. Market Revenue and Forecast, by Material (2020-2032)

11.4.2. Market Revenue and Forecast, by Service (2020-2032)

11.4.3. Market Revenue and Forecast, by End-use (2020-2032)

11.4.4. GCC

11.4.4.1. Market Revenue and Forecast, by Material (2020-2032)

11.4.4.2. Market Revenue and Forecast, by Service (2020-2032)

11.4.4.3. Market Revenue and Forecast, by End-use (2020-2032)

11.4.5. North Africa

11.4.5.1. Market Revenue and Forecast, by Material (2020-2032)

11.4.5.2. Market Revenue and Forecast, by Service (2020-2032)

11.4.5.3. Market Revenue and Forecast, by End-use (2020-2032)

11.4.6. South Africa

11.4.6.1. Market Revenue and Forecast, by Material (2020-2032)

11.4.6.2. Market Revenue and Forecast, by Service (2020-2032)

11.4.6.3. Market Revenue and Forecast, by End-use (2020-2032)

11.4.7. Rest of MEA

11.4.7.1. Market Revenue and Forecast, by Material (2020-2032)

11.4.7.2. Market Revenue and Forecast, by Service (2020-2032)

11.4.7.3. Market Revenue and Forecast, by End-use (2020-2032)

11.5. Latin America

11.5.1. Market Revenue and Forecast, by Material (2020-2032)

11.5.2. Market Revenue and Forecast, by Service (2020-2032)

11.5.3. Market Revenue and Forecast, by End-use (2020-2032)

11.5.4. Brazil

11.5.4.1. Market Revenue and Forecast, by Material (2020-2032)

11.5.4.2. Market Revenue and Forecast, by Service (2020-2032)

11.5.4.3. Market Revenue and Forecast, by End-use (2020-2032)

11.5.5. Rest of LATAM

11.5.5.1. Market Revenue and Forecast, by Material (2020-2032)

11.5.5.2. Market Revenue and Forecast, by Service (2020-2032)

11.5.5.3. Market Revenue and Forecast, by End-use (2020-2032)

Chapter 12. Company Profiles

12.1. ASB Industries (Hannecard Roller Coatings; Inc)

12.1.1. Company Overview

12.1.2. Product Offerings

12.1.3. Financial Performance

12.1.4. Recent Initiatives

12.2. Bodycote plc

12.2.1. Company Overview

12.2.2. Product Offerings

12.2.3. Financial Performance

12.2.4. Recent Initiatives

12.3. Flame Spray Technologies BV

12.3.1. Company Overview

12.3.2. Product Offerings

12.3.3. Financial Performance

12.3.4. Recent Initiatives

12.4. Plasma Giken Co., Ltd.

12.4.1. Company Overview

12.4.2. Product Offerings

12.4.3. Financial Performance

12.4.4. Recent Initiatives

12.5. VRC Metal Systems

12.5.1. Company Overview

12.5.2. Product Offerings

12.5.3. Financial Performance

12.5.4. Recent Initiatives

12.6. CenterLine (Windsor) Limited

12.6.1. Company Overview

12.6.2. Product Offerings

12.6.3. Financial Performance

12.6.4. Recent Initiatives

12.7. WWG Engineering Pte. Ltd.

12.7.1. Company Overview

12.7.2. Product Offerings

12.7.3. Financial Performance

12.7.4. Recent Initiatives

12.8. Praxair S.T. Technology, Inc.

12.8.1. Company Overview

12.8.2. Product Offerings

12.8.3. Financial Performance

12.8.4. Recent Initiatives

12.9. Impact Innovations GmbH

12.9.1. Company Overview

12.9.2. Product Offerings

12.9.3. Financial Performance

12.9.4. Recent Initiatives

12.10. Concurrent Technologies Corporation

12.10.1. Company Overview

12.10.2. Product Offerings

12.10.3. Financial Performance

12.10.4. Recent Initiatives

Chapter 13. Research Methodology

13.1. Primary Research

13.2. Secondary Research

13.3. Assumptions

Chapter 14. Appendix

14.1. About Us

14.2. Glossary of Terms

Cross-segment Market Size and Analysis for

Mentioned Segments

Additional Company Profiles (Upto 5 With No Cost)

Additional Countries (Apart From Mentioned Countries)

Country/Region-specific Report

Go To Market Strategy

Region Specific Market DynamicsRegion Level Market Share Import Export AnalysisProduction AnalysisOthers

Cross-segment Market Size and Analysis for

Mentioned Segments

Additional Company Profiles (Upto 5 With No Cost)

Additional Countries (Apart From Mentioned Countries)

Country/Region-specific Report

Go To Market Strategy

Region Specific Market DynamicsRegion Level Market Share Import Export AnalysisProduction AnalysisOthers