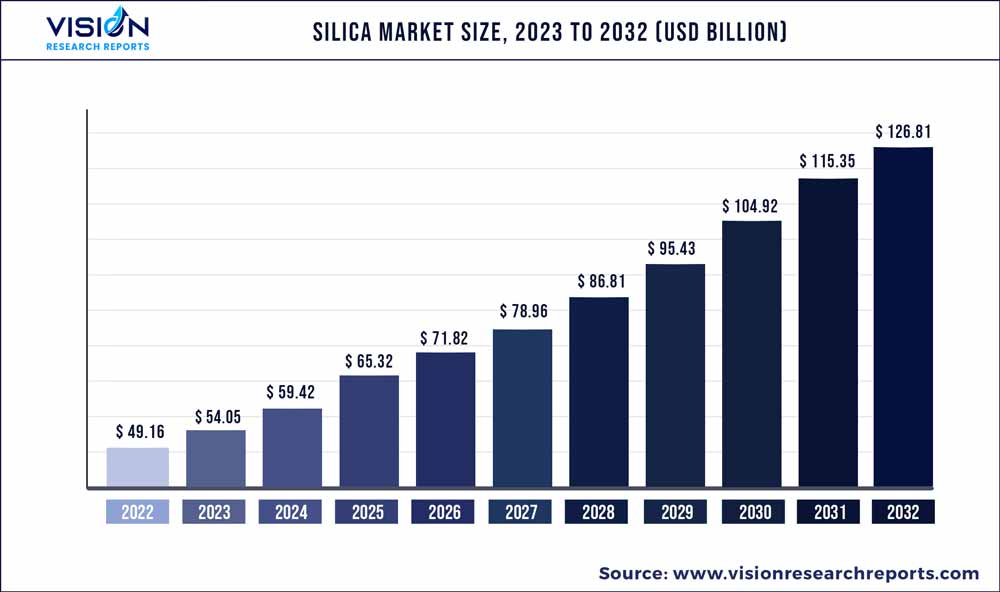

The global silica market was surpassed at USD 49.16 billion in 2022 and is expected to hit around USD 126.81 billion by 2032, growing at a CAGR of 9.94% from 2023 to 2032.

Key Pointers

Report Scope of the Silica Market

| Report Coverage | Details |

| Market Size in 2022 | USD 49.16 billion |

| Revenue Forecast by 2032 | USD 126.81 billion |

| Growth rate from 2023 to 2032 | CAGR of 9.94% |

| Base Year | 2022 |

| Forecast Period | 2023 to 2032 |

| Market Analysis (Terms Used) | Value (US$ Million/Billion) or (Volume/Units) |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Companies Covered | Evonik Industries; PPG Industries; Wacker Chemie AG; AkzoNobel N.V.; Tosoh Corporation; Cabot Corporation; Solvay SA, Oriental Silicas Corporation, Nissan Chemical Corporation, Kemira Oyj, Imersys S.A., W.R. Grace & Co. |

Precipitated silica, fumed silica, silica gels & sols, and silica fumes are considered in this report. The rising demand for silica from rubber industry is the primary factor driving the market growth. Silica provided higher abrasion resistance, tensile strength, and flex fatigue properties to rubber products. It is widely used in tire applications, owing to its ability to improve the bond & tear resistance between rubber tire and metallic reinforcements. The increase in demand for tires is mainly driven by rising automotive production, especially in countries such as India, China, Indonesia, South Korea, Japan, Malaysia, Taiwan, Mexico, U.S., and Germany.

Rapid economic growth, increasing government spending, advancements in road infrastructure, and increasing inclination of consumers toward personal conveyance are expected to boost demand for automobiles, thereby propelling the market growth. For instance, as Japan prepares itself to host the World Expo in Osaka, Japan, in 2025, the country's construction sector is expected to experience a boom. The 61-story, 390-meter office tower that is part of the Yaesu redevelopment project is expected to be finished between 2023 and 2032.

Moreover, the growth of silica market is driven by its increasing application in construction industry. Post-COVID-19 the construction industry has recovered rapidly and has helped balancing the market. Increasing demand for high quality concrete is driving the market is anticipated to continue in the forecast period. On the account of the growing construction industry in the emerging economies of Asia Pacific are expected to propel the paints & coatings industry and positively affect the market. For instance, according to the Shanghai project, China has announced to invest $1.43 trillion over five years, until 2025. Guangzhou has planned 16 new construction projects for USD 8.1 billion.

Silica fumes are majorly used in the concrete industry in order to impart strength and durability in concrete. The market is driven by the growth of the global construction sector. For instance, the construction market in Asia is expected to expand at a significant pace over the forecast period. High investment in the construction and infrastructure sectors across Southeast Asia is anticipated to positively affect product utilization through 2026.

Carbon black is one of the major substitutes of silica and acts as a restraint for market growth. Carbon black is used as a reinforcing agent in belts, tires, hoses, gaskets, diaphragms, air springs, bushings, chassis bumpers, and multiple types of boots, pads, wiper blades, and conveyor wheels. However, green tire manufacturers are replacing carbon black with silica on account of its eco-friendly benefits and stronger performance as opposed to carbon black. This is expected to have a positive impact on the market.

Application Insights

Based on application, rubber segment revenue accounted for a revenue share of over 33.02% of the global market 2022. Precipitated silica is extensively used in the rubber industry, particularly as a reinforcement filler in the manufacturing of tires. The specialized rubber compound, which is used in tires, is composed of various materials including natural as well as synthetic rubber.

Silica, when blended with tire rubber, helps reduce rolling resistance while simultaneously increasing the grip of tires. As a result, the adoption of silica in tires can reduce fuel consumption of a vehicle by about 7.0%. The share of low rolling-resistance tires reached 45.0% in 2021 from 15.0% in 2011. This trend is expected to continue on account of favorable government regulations in the tire industry.

Oral care application is estimated to expand at a CAGR of 8.96% over the forecast period. In oral care, silica gels & sols is commonly used as a thickening additive in toothpaste. Silica gels and sols are commonly used as a thickening additive in toothpaste. They are also used to provide cleaning properties to toothpaste. Increasing global demand for whitening toothpaste is likely to fuel product demand in oral care.

In agrochemicals, the product is used in liquid as well as solid formulations. It is used to deliver visco-elastic properties to the liquid formulation. It is also used as an anti-settling additive and a rheology modifier to prevent agglomeration of active ingredients, thereby avoiding sedimentation in liquid agrochemicals. As a result, it is suited to stabilize even highly acidic liquid formulations.

Regional Insights

Asia Pacific dominated the market with a revenue share of over 44.01% in 2022, owing to massive industrialization, increased construction spending, and increasing consumption of automobiles in the region. According to the International Organization of Motor Vehicle Manufacturers (OICA), Asia Pacific is the largest producer of motor vehicles. The region is projected to exhibit the fastest CAGR over the forecast period.

The growing automotive industry, coupled with the recovery of the construction sector in Central and South America, is predicted to have a positive impact on the silica market. Significant new investments by governments in the housing and public sector are predicted to propel the production of paints and coatings and sealants. This is estimated to drive the regional market.

North America acquired a revenue share of 21.64% in 2022. The expanding construction sector in the region is expected to drive demand for silica in applications such as concrete, paints and coatings, and adhesives and sealants. Rising demand for tires is significantly driving rubber applications in the U.S. For instance, according to the U.S. Tire Manufacturers Association (USTMA), tire shipments for passenger cars and trucks in the U.S. are poised to register significant growth over the next few years. This is anticipated to propel product demand in North America over the forecast period.

In Europe, the Paints Directive 2004/42/EC, framed by the European Commission, is aimed at limiting VOC emissions due to the use of organic solvents in architectural paints and varnishes as well as vehicle refinishing products. Hence, various initiatives are being taken to promote the use of eco-friendly materials in paints and coatings, thereby augmenting product demand. Moreover, Europe is one of the largest consumers of agrochemicals due to the high production and export of food grains. These factors are anticipated to boost demand for silica in the European agrochemical industry.

Silica Market Segmentations:

By Application

By Regional

Chapter 1. Introduction

1.1.Research Objective

1.2.Scope of the Study

1.3.Definition

Chapter 2. Research Methodology

2.1.Research Approach

2.2.Data Sources

2.3.Assumptions & Limitations

Chapter 3. Executive Summary

3.1.Market Snapshot

Chapter 4. Market Variables and Scope

4.1.Introduction

4.2.Market Classification and Scope

4.3.Industry Value Chain Analysis

4.3.1. Raw Material Procurement Analysis

4.3.2. Sales and Distribution Channel Analysis

4.3.3. Downstream Buyer Analysis

Chapter 5.COVID 19 Impact on Silica Market

5.1. COVID-19 Landscape: Silica Industry Impact

5.2. COVID 19 - Impact Assessment for the Industry

5.3. COVID 19 Impact: Global Major Government Policy

5.4.Market Trends and Opportunities in the COVID-19 Landscape

Chapter 6. Market Dynamics Analysis and Trends

6.1.Market Dynamics

6.1.1. Market Drivers

6.1.2. Market Restraints

6.1.3. Market Opportunities

6.2.Porter’s Five Forces Analysis

6.2.1. Bargaining power of suppliers

6.2.2. Bargaining power of buyers

6.2.3. Threat of substitute

6.2.4. Threat of new entrants

6.2.5. Degree of competition

Chapter 7. Competitive Landscape

7.1.1. Company Market Share/Positioning Analysis

7.1.2. Key Strategies Adopted by Players

7.1.3. Vendor Landscape

7.1.3.1.List of Suppliers

7.1.3.2.List of Buyers

Chapter 8. Global Silica Market, By Application

8.1.Silica Market, by Application Type, 2023-2032

8.1.1. Rubber

8.1.1.1.Market Revenue and Forecast (2020-2032)

8.1.2. Construction

8.1.2.1.Market Revenue and Forecast (2020-2032)

8.1.3. Agrochemicals

8.1.3.1.Market Revenue and Forecast (2020-2032)

8.1.4. Oral care

8.1.4.1.Market Revenue and Forecast (2020-2032)

8.1.5. Food & Feed

8.1.5.1.Market Revenue and Forecast (2020-2032)

8.1.6. Others

8.1.6.1.Market Revenue and Forecast (2020-2032)

Chapter 9. Global Silica Market, Regional Estimates and Trend Forecast

9.1. North America

9.1.1. Market Revenue and Forecast, by Application (2020-2032)

9.1.2. U.S.

9.1.2.1. Market Revenue and Forecast, by Application (2020-2032)

9.1.3. Rest of North America

9.1.3.1. Market Revenue and Forecast, by Application (2020-2032)

9.2. Europe

9.2.1. Market Revenue and Forecast, by Application (2020-2032)

9.2.2. UK

9.2.2.1. Market Revenue and Forecast, by Application (2020-2032)

9.2.3. Germany

9.2.3.1. Market Revenue and Forecast, by Application (2020-2032)

9.2.4. France

9.2.4.1. Market Revenue and Forecast, by Application (2020-2032)

9.2.5. Rest of Europe

9.2.5.1. Market Revenue and Forecast, by Application (2020-2032)

9.3. APAC

9.3.1. Market Revenue and Forecast, by Application (2020-2032)

9.3.2. India

9.3.2.1. Market Revenue and Forecast, by Application (2020-2032)

9.3.3. China

9.3.3.1. Market Revenue and Forecast, by Application (2020-2032)

9.3.4. Japan

9.3.4.1. Market Revenue and Forecast, by Application (2020-2032)

9.3.5. Rest of APAC

9.3.5.1. Market Revenue and Forecast, by Application (2020-2032)

9.4. MEA

9.4.1. Market Revenue and Forecast, by Application (2020-2032)

9.4.2. GCC

9.4.2.1. Market Revenue and Forecast, by Application (2020-2032)

9.4.3. North Africa

9.4.3.1. Market Revenue and Forecast, by Application (2020-2032)

9.4.4. South Africa

9.4.4.1. Market Revenue and Forecast, by Application (2020-2032)

9.4.5. Rest of MEA

9.4.5.1. Market Revenue and Forecast, by Application (2020-2032)

9.5. Latin America

9.5.1. Market Revenue and Forecast, by Application (2020-2032)

9.5.2. Brazil

9.5.2.1. Market Revenue and Forecast, by Application (2020-2032)

9.5.3. Rest of LATAM

9.5.3.1. Market Revenue and Forecast, by Application (2020-2032)

Chapter 10.Company Profiles

10.1. Evonik Industries

10.1.1.Company Overview

10.1.2.Product Offerings

10.1.3.Financial Performance

10.1.4.Recent Initiatives

10.2. PPG Industries

10.2.1.Company Overview

10.2.2.Product Offerings

10.2.3.Financial Performance

10.2.4.Recent Initiatives

10.3. Wacker Chemie AG

10.3.1.Company Overview

10.3.2.Product Offerings

10.3.3.Financial Performance

10.3.4.Recent Initiatives

10.4. AkzoNobel N.V.

10.4.1.Company Overview

10.4.2.Product Offerings

10.4.3.Financial Performance

10.4.4.Recent Initiatives

10.5. Tosoh Corporation

10.5.1.Company Overview

10.5.2.Product Offerings

10.5.3.Financial Performance

10.5.4.Recent Initiatives

10.6. Cabot Corporation

10.6.1.Company Overview

10.6.2.Product Offerings

10.6.3.Financial Performance

10.6.4.Recent Initiatives

10.7. Solvay SA

10.7.1.Company Overview

10.7.2.Product Offerings

10.7.3.Financial Performance

10.7.4.Recent Initiatives

10.8. Oriental Silicas Corporation

10.8.1.Company Overview

10.8.2.Product Offerings

10.8.3.Financial Performance

10.8.4.Recent Initiatives

10.9. Nissan Chemical Corporation

10.9.1.Company Overview

10.9.2.Product Offerings

10.9.3.Financial Performance

10.9.4.Recent Initiatives

10.10. Kemira Oyj

10.10.1. Company Overview

10.10.2. Product Offerings

10.10.3. Financial Performance

10.10.4. Recent Initiatives

Chapter 11.Research Methodology

11.1.Primary Research

11.2.Secondary Research

11.3.Assumptions

Chapter 12.Appendix

12.1. About Us

12.2. Glossary of Terms

Cross-segment Market Size and Analysis for

Mentioned Segments

Additional Company Profiles (Upto 5 With No Cost)

Additional Countries (Apart From Mentioned Countries)

Country/Region-specific Report

Go To Market Strategy

Region Specific Market DynamicsRegion Level Market Share Import Export AnalysisProduction AnalysisOthers

Cross-segment Market Size and Analysis for

Mentioned Segments

Additional Company Profiles (Upto 5 With No Cost)

Additional Countries (Apart From Mentioned Countries)

Country/Region-specific Report

Go To Market Strategy

Region Specific Market DynamicsRegion Level Market Share Import Export AnalysisProduction AnalysisOthers