U.S. & Europe Aluminum Foil Market Size, Growth, Trends | Report 2023-2032

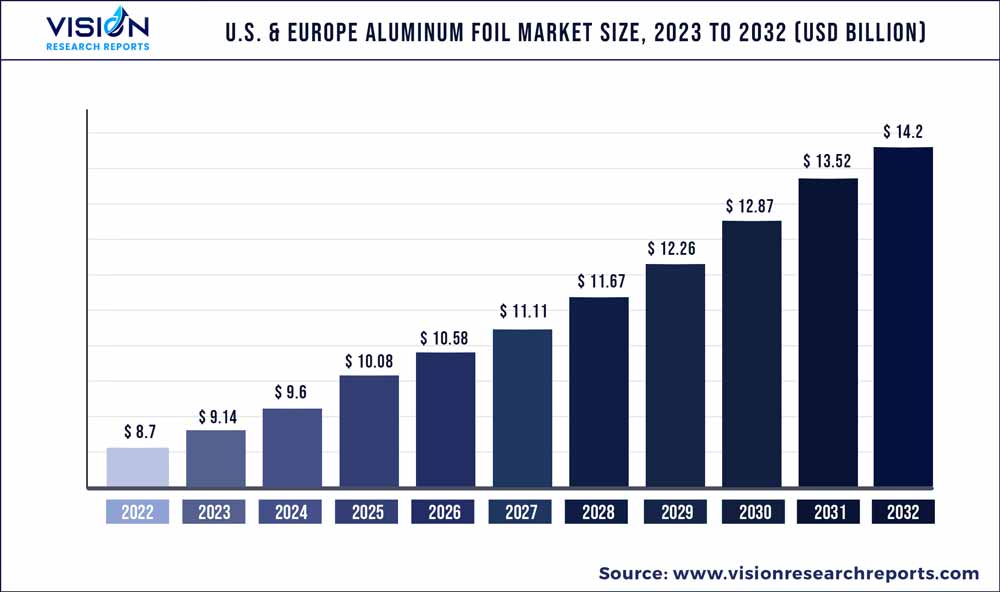

The U.S. & Europe aluminum foil market was surpassed at USD 8.7 billion in 2022 and is expected to hit around USD 14.2 billion by 2032, growing at a CAGR of 5.02% from 2023 to 2032.

Key Pointers

Report Scope of the U.S. & Europe Aluminum Foil Market

| Report Coverage | Details |

| Market Size in 2022 | USD 8.7 billion |

| Revenue Forecast by 2032 | USD 14.2 billion |

| Growth rate from 2023 to 2032 | CAGR of 5.02% |

| Base Year | 2022 |

| Forecast Period | 2023 to 2032 |

| Market Analysis (Terms Used) | Value (US$ Million/Billion) or (Volume/Units) |

| Companies Covered | Dongwon Systems; GLS Group; Hangzhou Dingsheng Industrial Group Co. Ltd.; Hindalco Industries Ltd.; Jindal (India) Ltd.; LKSB Aluminum Foils; Nanshan; Qualityfoil Sarl; Raviraj Foils Ltd.; Shyam Metalics; SNTO (Suntown Technology Group Corp. Ltd.); Sparsh Industries |

Growing income levels and improving economic conditions will support market growth in both regions. In addition, the growing Electrical Vehicle (EV) industry is anticipated to significantly impact market development. Based on end-uses, the market is segmented into packaging and industrial. The product finds use in lithium-ion batteries in the production of cathode foil. Hence, the increasing production of EVs is anticipated to drive product consumption in electric battery applications.

For instance, in December 2021, VinFast announced an investment of USD 173.7 million to build an electric battery manufacturing plant in Hai Phong, Vietnam. The facility is expected to have an annual production capacity of 100,000 units. The packaging end-use industry dominated the market in 2022. Aluminum foil-based products are widely used in packaging end-uses as they protect packed goods against light, oxygen, moisture, and bacteria. They are primarily used for the packaging of tobacco, food & beverages, pharmaceuticals, and cosmetics. Aluminum foil is considered an ideal material for packaging food & beverages as it is lightweight, easily recyclable, and flexible. Thus, the rising investments in the food & beverage sector are expected to augment the market growth over the forecast period.

For instance, in September 2021, PepsiCo laid the foundation for constructing one of its largest food manufacturing facilities in Poland. The project is worth USD 220 million, and the construction is expected to get completed by 2025. The investment is aimed at expanding the production capacity of its food portfolio, including Doritos corn chips, and Lay’s fried & oven-baked chips, to meet the growing demand. The market is competitive with the presence of numerous players. Expansion is one of the key strategies adopted by the key players. For instance, in August 2022, LOTTE Chemicals established a joint venture facility with LOTTE Aluminum for producing aluminum foil. The new facility will produce cathode foil (ultra-thin aluminum foil) to be used in EV batteries. The facility is expected to have an annual production capacity of 36 kilotons.

Product Insights

On the basis of products, the industry has been further categorized into wrapper foils, container foils, foil lids, pouches, blister packs, and others. The wrapper foils segment dominated the industry in 2022 and accounted for the maximum share of more than 22.47% of the overall revenue. The large share of the segment can be attributed to the growing demand for wrapper foils in food delivery businesses, restaurants, households, and other end-uses.

Their demand has witnessed a surge, especially after the pandemic, as the masses across the world made efforts to minimize the risk of getting affected by coronavirus by relying on packaged food delivery services. The foil lids segment is estimated to account for the second-largest share of the market. The increasing investments in the global pharmaceutical sector are expected to augment the demand for aluminum foil lids over the forecast period. For instance, in August 2021, Amgen Inc. invested USD 550 million in the construction of a drug substance production plant in North Carolina, U.S.

End-use Insights

The packaging segment held the largest share of over 65.02% in 2022 of the overall market. It is considered an ideal material for packaging food & beverages as it is lightweight, easily recyclable, and flexible. The rising investments in the food & beverage sector are expected to augment the demand for aluminum foil over the forecast period. For instance, in September 2021, PepsiCo laid the foundation for constructing one of its largest food manufacturing facilities in Poland. The project is worth USD 220 million, and the construction is expected to get completed by 2025.

The other end-use of aluminum foil is the industrial segment, which is further categorized into HVAC, EV battery, and other industrial end-uses. It is widely used for the manufacturing of finstock for air conditioners, heat exchangers, and car radiators. The rapid growth of the building & construction industry is expected to propel the demand for HVAC systems over the forecast period. For instance, in January 2022, the Indonesian parliament passed a law, the Capital City Bill, to build the new capital city in East Kalimantan province. The country is anticipated to invest USD 35 billion in new capital city construction, which is expected to be completed by 2024.

U.S. & Europe Aluminum Foil Market Segmentations:

By Product

By End-use

Chapter 1. Introduction

1.1. Research Objective

1.2. Scope of the Study

1.3. Definition

Chapter 2. Research Methodology

2.1. Research Approach

2.2. Data Sources

2.3. Assumptions & Limitations

Chapter 3. Executive Summary

3.1. Market Snapshot

Chapter 4. Market Variables and Scope

4.1. Introduction

4.2. Market Classification and Scope

4.3. Industry Value Chain Analysis

4.3.1. Raw Material Procurement Analysis

4.3.2. Sales and Distribution Channel Analysis

4.3.3. Downstream Buyer Analysis

Chapter 5. COVID 19 Impact on U.S. & Europe Aluminum Foil Market

5.1. COVID-19 Landscape: U.S. & Europe Aluminum Foil Industry Impact

5.2. COVID 19 - Impact Assessment for the Industry

5.3. COVID 19 Impact: Major Government Policy

5.4. Market Trends and Opportunities in the COVID-19 Landscape

Chapter 6. Market Dynamics Analysis and Trends

6.1. Market Dynamics

6.1.1. Market Drivers

6.1.2. Market Restraints

6.1.3. Market Opportunities

6.2. Porter’s Five Forces Analysis

6.2.1. Bargaining power of suppliers

6.2.2. Bargaining power of buyers

6.2.3. Threat of substitute

6.2.4. Threat of new entrants

6.2.5. Degree of competition

Chapter 7. Competitive Landscape

7.1.1. Company Market Share/Positioning Analysis

7.1.2. Key Strategies Adopted by Players

7.1.3. Vendor Landscape

7.1.3.1. List of Suppliers

7.1.3.2. List of Buyers

Chapter 8. U.S. & Europe Aluminum Foil Market, By Product

8.1. U.S. & Europe Aluminum Foil Market, by Product, 2023-2032

8.1.1. Wrapper Foils

8.1.1.1. Market Revenue and Forecast (2020-2032)

8.1.2. Container Foils

8.1.2.1. Market Revenue and Forecast (2020-2032)

8.1.3. Foil Lids

8.1.3.1. Market Revenue and Forecast (2020-2032)

8.1.4. Pouches

8.1.4.1. Market Revenue and Forecast (2020-2032)

8.1.5. Blister Packs

8.1.5.1. Market Revenue and Forecast (2020-2032)

8.1.6. Others

8.1.6.1. Market Revenue and Forecast (2020-2032)

Chapter 9. U.S. & Europe Aluminum Foil Market, By End-use

9.1. U.S. & Europe Aluminum Foil Market, by End-use, 2023-2032

9.1.1. Packaging

9.1.1.1. Market Revenue and Forecast (2020-2032)

9.1.2. Industrial

9.1.2.1. Market Revenue and Forecast (2020-2032)

Chapter 10. U.S. & Europe Aluminum Foil Market, Regional Estimates and Trend Forecast

10.1. U.S.

10.1.1. Market Revenue and Forecast, by Product (2020-2032)

10.1.2. Market Revenue and Forecast, by End-use (2020-2032)

10.2. Europe

10.2.1. Market Revenue and Forecast, by Product (2020-2032)

10.2.2. Market Revenue and Forecast, by End-use (2020-2032)

10.2.3. UK

10.2.3.1. Market Revenue and Forecast, by Product (2020-2032)

10.2.3.2. Market Revenue and Forecast, by End-use (2020-2032)

10.2.4. Germany

10.2.4.1. Market Revenue and Forecast, by Product (2020-2032)

10.2.4.2. Market Revenue and Forecast, by End-use (2020-2032)

10.2.5. France

10.2.5.1. Market Revenue and Forecast, by Product (2020-2032)

10.2.5.2. Market Revenue and Forecast, by End-use (2020-2032)

10.2.6. Rest of Europe

10.2.6.1. Market Revenue and Forecast, by Product (2020-2032)

10.2.6.2. Market Revenue and Forecast, by End-use (2020-2032)

Chapter 11. Company Profiles

11.1. Dongwon Systems

11.1.1. Company Overview

11.1.2. Product Offerings

11.1.3. Financial Performance

11.1.4. Recent Initiatives

11.2. GLS Group

11.2.1. Company Overview

11.2.2. Product Offerings

11.2.3. Financial Performance

11.2.4. Recent Initiatives

11.3. Hangzhou Dingsheng Industrial Group Co. Ltd.

11.3.1. Company Overview

11.3.2. Product Offerings

11.3.3. Financial Performance

11.3.4. Recent Initiatives

11.4. Hindalco Industries Ltd.

11.4.1. Company Overview

11.4.2. Product Offerings

11.4.3. Financial Performance

11.4.4. LTE Scientific

11.5. Jindal (India) Ltd.

11.5.1. Company Overview

11.5.2. Product Offerings

11.5.3. Financial Performance

11.5.4. Recent Initiatives

11.6. LKSB Aluminum Foils

11.6.1. Company Overview

11.6.2. Product Offerings

11.6.3. Financial Performance

11.6.4. Recent Initiatives

11.7. Nanshan

11.7.1. Company Overview

11.7.2. Product Offerings

11.7.3. Financial Performance

11.7.4. Recent Initiatives

11.8. Qualityfoil Sarl

11.8.1. Company Overview

11.8.2. Product Offerings

11.8.3. Financial Performance

11.8.4. Recent Initiatives

11.9. Raviraj Foils Ltd.

11.9.1. Company Overview

11.9.2. Product Offerings

11.9.3. Financial Performance

11.9.4. Recent Initiatives

11.10. Shyam Metalics

11.10.1. Company Overview

11.10.2. Product Offerings

11.10.3. Financial Performance

11.10.4. Recent Initiatives

Chapter 12. Research Methodology

12.1. Primary Research

12.2. Secondary Research

12.3. Assumptions

Chapter 13. Appendix

13.1. About Us

13.2. Glossary of Terms

Cross-segment Market Size and Analysis for

Mentioned Segments

Additional Company Profiles (Upto 5 With No Cost)

Additional Countries (Apart From Mentioned Countries)

Country/Region-specific Report

Go To Market Strategy

Region Specific Market DynamicsRegion Level Market Share Import Export AnalysisProduction AnalysisOthers

Cross-segment Market Size and Analysis for

Mentioned Segments

Additional Company Profiles (Upto 5 With No Cost)

Additional Countries (Apart From Mentioned Countries)

Country/Region-specific Report

Go To Market Strategy

Region Specific Market DynamicsRegion Level Market Share Import Export AnalysisProduction AnalysisOthers